How to get out of debt in 5 simple steps

Imagine what you could do with your income if you had no payments going out each month.

Anything you want!

Getting out of debt is about three things: financial security, regaining control of your income and giving yourself more choices in life. When you don’t have to worry about debt payments or being able to cover the necessities, your income truly becomes your money – allowing you to save, create more opportunities for yourself and do more of what you love in life.

Eliminating debt from your life will give you an extraordinary sense of freedom and peace of mind. You’ll be able to spend your own money without cringing or worrying about the next bill. Your money will actually be your money. And most importantly, you’ll have the financial security and stability to handle whatever challenges come your way.

Getting there isn’t easy, but with the right mindset and plan, you can eliminate your debt and all the stress, trouble and damage that comes with it.

Prioritizing your debts

Different types of debt impact your financial life differently. When it comes to eliminating your debt obligations, it’s important to prioritize which ones you focus on paying off first.

While no debt is necessarily good, different types of debt can be considered good or bad, depending on what they are and how they impact your credit and overall financial life. What makes many types of debt good or bad is simply how you handle them.

When creating a plan to pay off your debt, it’s important to prioritize those that are causing you the most damage and costing you the most money.

What is good debt?

A mortgage is considered good debt, because it’s an investment in something that increases in value (or should), and mortgages typically carry a low interest rate. Student loans are also considered good debt, because you’re investing in your future career in order to get a better, higher-paying job down the road – and they also typically have lower interest rates. So when you start putting together your repayment plan, these debts are really your last priority.

Read more: 4 ways good debt can improve your financial life

What is bad debt?

Bad debt is any expensive financial obligation that weighs down your overall financial situation – which means debt that carries a high or variable interest rate, especially when used for unnecessary spending or to make a big purchase that loses value.

Bad debt is also debt that could have a good impact on your financial situation but has been handled in a bad way. Credit cards are a great example of this, because the card itself is not the problem, it’s how you use it that can cause you problems. In fact, using a credit card and paying off the full balance each month actually helps your credit. But since credit cards carry high interest rates, it’s when you can’t pay the bill in full when a credit card starts to cause you big financial trouble.

Examples of bad debt include credit cards that carry a balance, high-interest store cards, car loans and payday loans.

See more on good debt vs. bad debt.

Preparing yourself mentally

Getting out of debt is no easy task – it takes a lot of effort, focus and most importantly, change. Personal finance is 20% knowledge and 80% behavior. Paying off debt will most certainly require you to make some changes, sometimes big ones, and continuing to remind yourself why you’re doing it will help keep you motivated along the way.

Many people choose to live with the stress and burden of debt because they’re too afraid to face the reality of their situation. But facing it is the only way to get out from under the chokehold that debt has on you and your life – so that you can begin to live life on your own terms. Your situation will never change until you decide to do something about it – and once you do, your life will improve in more ways than you ever could have imagined.

How to pay off your debt in 5 steps

1. Stop the bleeding

Stop borrowing money! The first step to getting out of debt is to stop racking up more debt. No more loans. No more big purchases you can’t pay for in cash. Cut up your credit cards, freeze them – I don’t care what you do, just stop using them.

Meanwhile, don’t ignore the damage that’s already been done. The cards may be gone, but the bills are not. It’s crucial that you continue to make the minimum payment on each debt every month. This will prevent them from causing more damage to your credit.

A great way to stop the bleeding and rein in overspending is to go to a cash-only budget. If you can’t pay for it in cash, you don’t buy it.

2. Create a budget & free up some cash

What you’re doing isn’t working, so it’s time to make some changes. Your spending habits need total makeover and the best way to do this is to start tracking where your money is actually going. Sticking to a budget is crucial in order to reduce your spending and free up the money you’ll need to pay off your debt. And keep in mind, your budget will be based on your total take-home pay – the cash you’re bringing in each month after taxes and any 401k/retirement contributions.

Start by adding up all of your current expenses. Go through the past three months of statements and figure out about how much you’re spending on everything each month, including housing, bills, food, discretionary spending (going out, random purchases, gifts, clothing etc.), debt obligations – anything you spend money on.

Here are a few examples of budget categories to consider:

Housing (including utilities, HOA fees – any expenses related to housing)

Healthcare

Food

Insurance

Transportation

Savings

Debt

Discretionary spending (entertainment, subscriptions, shopping, gifts etc.)

Extra expenses (anything else + expenses unique to your life and situation)

Break out your expenses into categories – for example, housing can include rent/mortgage, renter’s/homeowner’s insurance and utilities. Discretionary spending is anything you could live without – this could include your cell phone bill, subscriptions like Amazon Prime or Spotify, shopping, going out, gifts etc.

Then with everything in front of you, start adding up all of the expenses in each category. If you’re using the past three months, take the average.

Budget Recommendations

In order to create a budget, you need to have an idea of how much you should be spending on everything.

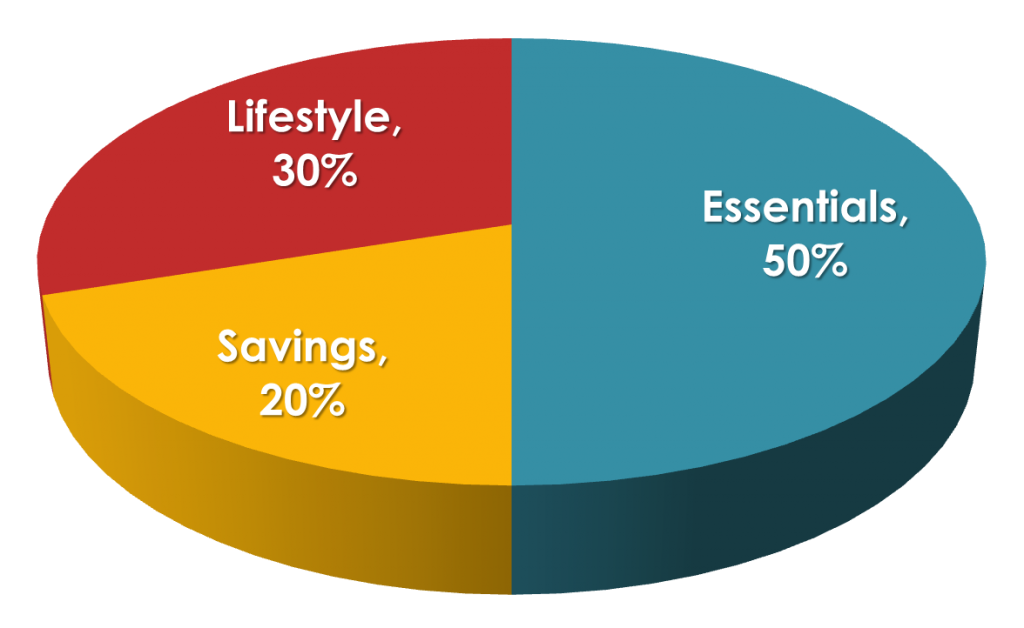

I like to use the 50/30/20 budgeting method, which is a pretty common one. Here’s how it works:

50% needs: 50% of your monthly take-home pay should go toward everything you need, so things like housing, food/groceries, healthcare costs and transportation.

30% wants: 30% of your income should cover any wants — so things you can survive without — which includes things like your cell phone, entertainment, subscriptions, shopping, gifts etc.

20% savings & debt: The remaining 20% of your income should go toward savings (emergency, retirement and long-term) and any debt obligations you have.

This will give you a baseline to start with — keep in mind that these percentages will change once you begin reducing expenses, in order to free up money that will go toward debt.

This gives you a good starting point and once you have all of your expenses in front of you, you’ll be able to determine how far off you are and where you need to start making some changes.

Check out my budgeting guide for a more in-depth look at budgeting.

3. Reduce expenses and/or find ways to earn more

Reducing spending

Once you have a budget and a framework for how much you should be spending, then it’s time to start reducing expenses – big and small.

First look at any expenses that are relatively easy to reduce – shop for cheaper insurance (car and home), look for a cheaper cell phone plan, eliminate or combine subscriptions. If you spend a lot on going out, it’s probably time to eat at home more often. Then for any expenses that vary each month (groceries, shopping, going out etc.), set a specific amount for each month and do not go over that amount. Take out cash to cover these areas of spending. That will force you to pick and choose and also find ways to save.

Any expense you can reduce will help you free up more cash that can go toward your debt. Making changes now is the only way to change your life down the road!

Create extra cash

Another way to free up cash to sell stuff. Get rid of that unnecessary clutter and make some cash on things you don’t use or need anymore. Be realistic and let it go! Once you’re financially stable, you’ll be able to afford to buy all new stuff – without cringing or worrying about how you’ll pay the bill.

Read more: 9 ways to find free money

Earn more money

Earning more money is another way to jumpstart your debt payoff plan. Whether it’s finding a new job, taking extra hours at work, taking on part-time work or hustling on the side – there are plenty of ways to earn extra cash that can be thrown at your debt.

Here’s a list of ways to make money on the side.

4. List out your debts

This can be pretty miserable, but it’s necessary in order to know exactly what you’re facing. So buck up and bite the bullet.

The easiest way to do this is to make two lists of all of your debt obligations: one that lists them by total owed and another by interest rate. Make sure to also include the minimum monthly payment amount for each one.

Once you reach this point, you’re ready to make a plan to get it all paid off!

5. Make a plan

Give yourself a timeline

Giving yourself a strict, and realistic, timeline will not only help you to stay on track, but it will also serve as a reminder that there is an end in sight. It’s much easier to tolerate certain changes when you know that it’s only temporary.

Your specific timeline is going to depend on how much you owe and how much you’re willing to sacrifice. Setting a goal to get your debt wiped out in 36 months or less is a great place to start. When your timeline starts to get longer than 36 months, it’s easy to lose focus and motivation

Choosing an approach

There are two common methods for how to approach paying off debt.

The first is called laddering. This is when you focus on the debt with the highest interest rate first, since that one is costing you the most money over time.

The second is the snowball method. This is when you focus on the debt with the smallest balance first and work your way up from there. So you list out your debts from smallest to largest and if two debts have similar balances, then you list the one with the higher interest rate first. You put all of your extra money toward the smallest balance, and then once that’s paid off, you take the money you were throwing at that debt, plus any extra, and put it toward the next smallest balance. Once that one is paid off, you take all that money, plus any extra, and apply it to the next smallest balance on the list, and so on. So as you work your way through your debts, each time one is paid off, you’re accumulating more money to put toward the next one.

Both methods have their benefits, so how do you decide what’s best for you!

Laddering takes a level of focus and diligence that most people don’t have. It will save you money in the long run, but it can be difficult to stay motivated since your debt with the highest interest rate may carry a very large balance – meaning it may take a while to see progress and get it paid down. And when it comes down to it, as long as your payoff plan doesn’t span several years, the total cost may not be much different.

With the snowball method, since you’re tackling your smallest balances first, you see progress very quickly. You get a mental boost each time you wipe out a debt, making it much easier to stay motivated and to stick to your plan.

Continue making minimum payments

Whether you choose laddering or the snowball method, it’s crucial that you continue to pay the minimum amount due every single month. This will allow you to minimize the damage while you work to get it all paid off.

Bonus: Get help when you need it!

If you’re struggling to get your plan together, or to even make your minimum payments, get some help! There are free resources available to help you create a plan that’s best for you and your situation. Visit NFCC.org for more information and to find resources in your area.